| |

This report addresses aspects such as prices, inventories, markets and Japaneses imports of the species that are detailed in the index.

1. ASIA

1.1 Japan

Northern bluefin tuna (Thunnus thynnus and Thunnus orientalis)

Southern bluefin tuna (Thunnus maccoyii)

Fresh

Prices

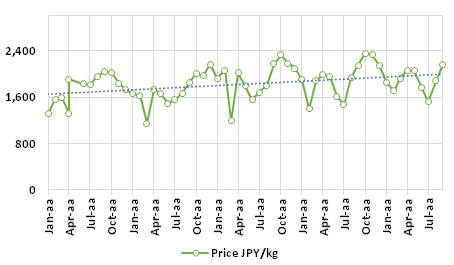

The average CIF price of fresh (Thunnus maccoyii, Thunnus thynnus and Thunnus orientalis) bluefin imported by Japan in September was JPY 2,166/kg, 16% higher than last month and 1% higher than September 2018. During the nine months, the average was JPY 1,838/kg, up 4% on that of the same period last year.

Table 1: Average price CIF at Japan Customs, in JPY/kg

|

Origin

|

Average price at Customs (JPY/kg)

|

% Variation

|

|

Sep/19

|

Aug/19

|

Sep/18

|

Sep/19 Aug/19

|

Sep/19 Sep/18

|

|

Spain

|

2,841

|

2,902

|

2,899

|

-2%

|

-2%

|

|

Italy

|

-

|

-

|

-

|

.

|

.

|

|

Malta

|

-

|

-

|

-

|

.

|

.

|

|

Greece

|

-

|

-

|

-

|

.

|

.

|

|

Turkey

|

2,225

|

-

|

-

|

.

|

.

|

|

USA

|

2,669

|

2,907

|

2,786

|

-8%

|

-4%

|

|

Mexico

|

2,289

|

2,144

|

2,090

|

7%

|

10%

|

|

Australia (SBFT)

|

1,156

|

1,496

|

1,232

|

-23%

|

-6%

|

Source: Japanese Customs

Graph 1: Average customs price of Japanese imports of fresh bluefin, 2015/2019, in JPY/kg

Source: Customs/FIS.com

Markets

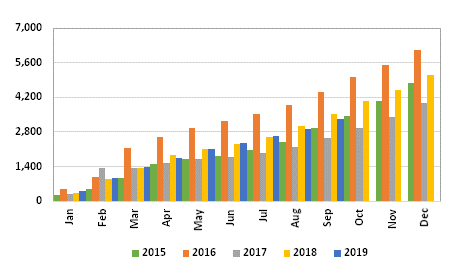

In September 459 tons of fresh bluefin were imported for a Japanese customs value of JPY 994 million.

These figures are 15% lower in volume and 2% in value compared to those registered the previous month. In relation to September last year, imports fell 17% in volume and value.

Graph 2: Japanese imports of fresh bluefin,2015/2019

Source: Customs/FIS.com

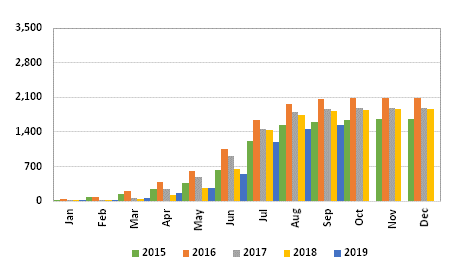

In the period, 4,838 tonnes were imported for JPY 8,891 million, down 9% in volume and 6% more in value than in the same period last year.

Graph 3: Cumulative monthly Japanese imports of fresh northern bluefin, 2015/2019, in tonnes

Source: Japanese Customs

El principal proveedor de bluefin del norte (Thunnus thynnus y/o Thunnus orientalis) en el periodo es Mexico con 2.489 toneladas y JPY 5.214 millones.

Graph 4: Imports of fresh southern bluefin, accumulated monthly, 2015/2019, in tonnes

Source: Japanese Customs

The main origin of fresh southern bluefin was New Zealand, 791 tons per JPY 1,138 million, followed by Australia with 702 t.

By DGA

www.fis.com

|

Print

Print